RELOCATING TO SWITZERLAND

- von Obrist Helps

- •

- 01 Juni, 2018

- •

WHICH INSURANCE DO I NEED?

Relocating to another country is never an easy decision to make and there are many reasons for going abroad: the partner, the family, the job and many more. Once decided and relocated to Switzerland, the first duty calls: A health insurance is compulsory in Switzerland. Obrist Helps gives as an independent insurance broker a good overview of the health insurance obligation in Switzerland and explains important models and differences.

In Switzerland the health insurance is mandatory

Every person living in Switzerland needs to hold a health insurance. Within three months after relocating to Switzerland and registering for residence, one must decide for one of the many health insurance companies and models. The service level of each insurance company, the chosen doctor's model, the franchise, the supplementary insurance and, last but not least, the health insurance premium should be adjusted to one's needs and state of health.

The basic insurance (compulsory)

The basic insurance is mandatory for every person living in Switzerland. You can not influence the duty to be health insured, but, for sure you can decide which health insurance company you decide to go for and you are also free to choose the doctor's model or the franchise options.

Franchise options

The franchise defines the amount, that needs to be payed by oneself, per calendar year, from one’s total health costs resulted by visits to the doctor and medicines.

Defined by the law, the following Franchise options are possible and are the same for each health insurance company: CHF 300 / CHF 500 / CHF 1000 / CHF 1500 / CHF 2000 / CHF 2500.

Once the amount of the chosen franchise is reached, 90% of the costs are borne by the health insurance company. 10% must be payed by the patient as a deductible.

The more often one uses medical services, the sooner a lower Franchise is recommended (for example CHF 300). Conversely, this means that, the highest franchise makes sense if one is visiting the doctor occasionally. The higher the franchise, the lower the monthly due, but one must always keep in mind, that in a case of emergency, having a high franchise, always a certain amount of money must be saved, to be able to pay unexpected costs.

Doctor models

- Free doctors choice: For every concern you can go to a doctor or specialist of your choice. This model is the most expensive model.

- Primary Care Physician / HMO Model: Any health concern must be going through the primary care physician or through the HMO Center (Health Maintenance Organization). If necessary, the primary care physician will refer the patient to a specialist. This is probably the most common model in Switzerland.

- Telephone model / Telemed: In order to be able to see a doctor or specialist, with this model one needs to call the health insurance first. This model is for sure the cheapest option.

Accident insurance

In Switzerland, a distinction is made between health insurance and accident insurance. If you have a job and work more than 8 hours per week, you are covered by the employer's accident insurance - even in the case of accidents outside of work. An inclusion of the accident insurance with the basic insurance is not necessary in this case. If your do not have a job, or work less than 8 hours per week, but also for children, accident insurance should be included.

Supplementary insurance (VVG)

It is not a must - but highly recommended. The supplementary insurance closes the gap to optimal insurance protection.

For example with the Hospital Insurance one may be insured for the general department, half-private department, private department and Flex models. Depending on the department, differences may arise between the responsible physicians and sharing of the hospital room with other patients.

Complementary medicine (such as homeopathy), medicines, emergency treatment abroad, transports, physiotherapy, contributions to fitness centers, glasses, contact lenses, etc. are offered in different types and coverages depending on the supplementary insurance package and constellation. Compare and, above all, a competent advice at this point is worthwhile.

Good to know

The insurance benefits of the basic insurance are identical and statutory with all health insurance companies. It exists a uniform service catalog, which must be fulfilled by each health insurance company in Switzerland.

The advisory service for insurance companies is for free and is included in the monthly insurance due, and as a result, there are usually no invoices from insurance advisors to customers.

Compare health insurances and ask for advice

It turns out that one has to think of many things when choosing a health insurance company. Despite nationwide requirement of a health insurance obligation, there are various differences for each insurance company.

When choosing the right franchise, doctor's model or supplementary insurance, it is advisable to consult an independent specialist in order to obtain correct and transparent advice.

Doman Obrist with Obrist Helps

is an independent insurance broker, helping his clients making the

right choice with their insurance. He is specialized in International

Local Hires. He is fluent in German and English.

Once, you have decided to relocate to Switzerland for business reasons, many expats do not pay enough attention on choosing accomodation for living in a city or village with a lower tax rate. It is understandable that, in fact, the choice of the apartment should mostly be located in a geographically advantageous location next to the workplace. But wouldn't it make sense to first calculate how much of your income is getting "lost" through taxes? In this blog we want to give examples of how important the choice of municipality may be for the different tax rates.

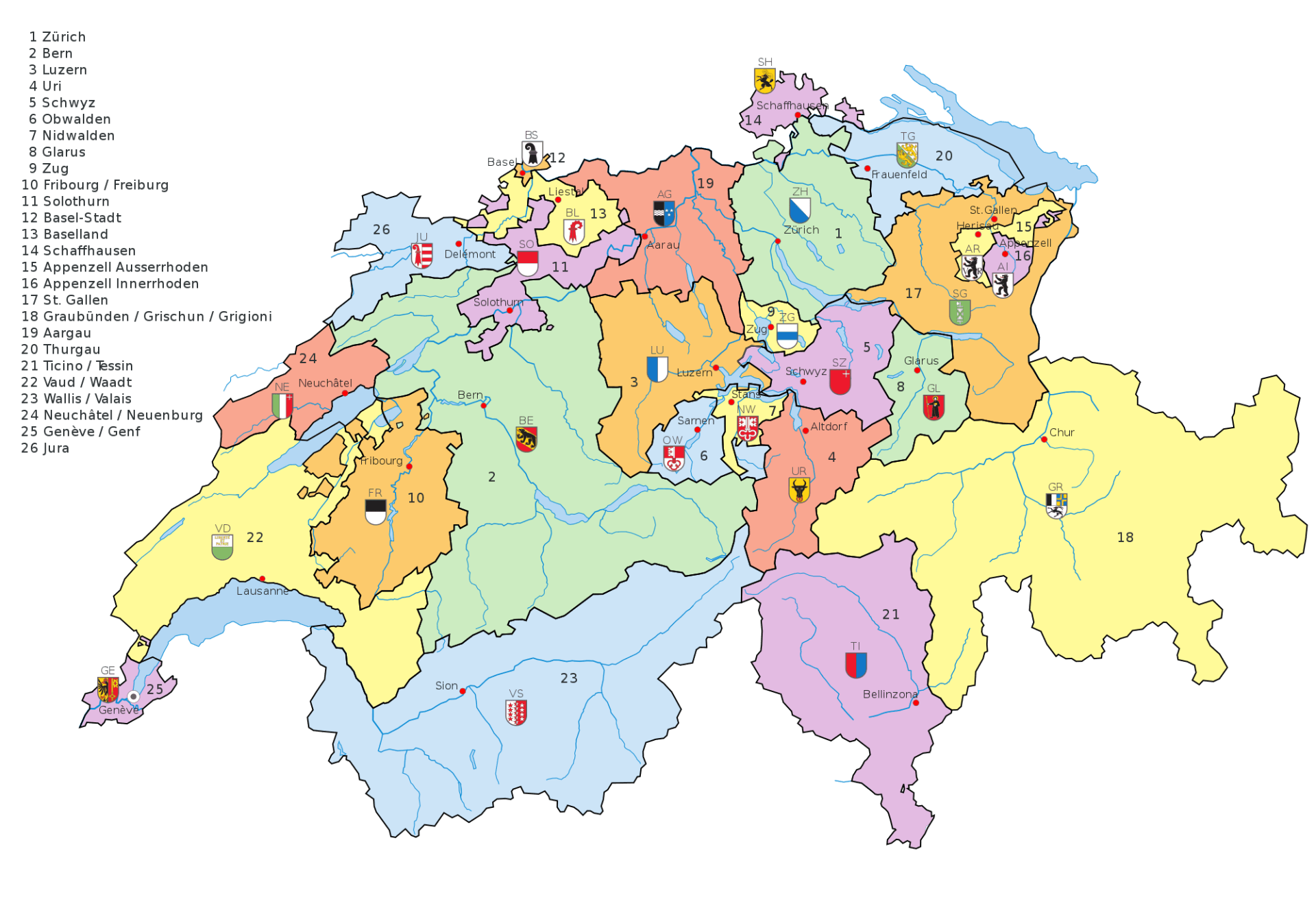

In Switzerland, there are two diffrent types of taxes. On the one hand we have the federal tax which remains the same for the whole nation. On the other hand, we have the canton & municipality tax, which may differ.

Example 1 (Zurich City)

Based on an income of CHF 120’000 net salary per annum and CHF 95’000 tax based salary, as a single person without church tax, you pay in Zurich CHF 5'845.00 for the Canton tax, which is equal to 100% (6.153 % from CHF 95’000). The city of Zürich has a tax rate of 119% which means, we add another CHF 6'955.55 for Zurich plus the “Personalsteuer” of CHF 24 which is in total CHF 12’824.55. In addition we add the federal tax which is CHF 2'544.-. All in all you end up with taxes of CHF 15’368.55 per year.

Example 2 (Kilchberg)

Contrary to Zurich (119%) the municipality rate is lower (72 %). Instead of CHF 6955.55 you “only” have to pay CHF 4'208.40 taxes for Kilchberg. In total you end up with taxes of CHF 12’621.40. You would save CHF 2747.15 on taxes.

Funfact :

In this example your flat could be CHF 228.90 more expensive in Kilchberg than in Zurich. So for example if you find a flat with an equal price in Kilchberg, you could safe the whole difference! That's a lot of money.

Example 3 (Wollerau, Canton Schwyz)

The equal share of 100% in Canton Schwyz amounts to CHF 3,128 for the same income. Calculated to 170% you end up with CHF 5'319 for the canton and 75% for municipality Wollerau which is CHF 2'347. Without the federal tax, you will pay CHF 7666 and plus CHF 2544 federal tax you end up with a total taxation of CHF 10’210.

Summary

- In Zurich City you would pay a total of CHF 15'369.

- In the canton of Zurich in Kilchberg you would pay CHF 12'621.

- In Canton Schwyz in Wollerau you would pay CHF 10'210.

The earlier you calculate your taxiation, the faster you can actively save money or spend it for whatever you wish for. Always remember that the higher your income, the greater the difference. Avoid hasty relocation plans without worrying about the tax issue. Perhaps it is "only" CHF 1,000 calculated for the whole year, but calculated for 10 years it means CHF 10,000, which you could have reinvested differently.

In der Schweiz gibt es zwei Arten von Steuern. Auf der einen Seite haben wir die Bundessteuer, die für die ganze Schweiz gleich ist. Auf der anderen Seite haben wir die Kantons- und Gemeindesteuer. Hier unterscheidet sich der Steuersatz.

Beispiel 1 (Stadt Zürich)

Ausgehend von einem Einkommen von 120'000 Nettogehalt und CHF 95'000 steuerpflichtigem Gehalt bezahlen Sie in Zürich als Einzelperson ohne Kirchensteuer für die Kantonssteuer CHF 5'845, was 100% entspricht (6.153 % ab CHF 95'000.00). Die Stadt Zürich hat einen Steuersatz von 119%, d.h. wir addieren weitere CHF 6'955.55 für Zürich plus die "Personalsteuer" von CHF 24, was insgesamt CHF 12'824.55 entspricht. Dazu kommt die Bundessteuer von CHF 2'544. Alles in allem ergibt sich eine Steuer von CHF 15'368.55.

Beispiel 2 (Kilchberg)

Im Gegensatz zu Zürich (119%) ist die Gemeindequote mit 72% deutlich niedriger. Statt CHF 6955.55 zahlen Sie "nur" CHF 4'208.40 Steuern für Kilchberg. Insgesamt fallen Steuern von CHF 12'621.40 an. Sie sparen CHF 2747.15 an Steuern.

Funfact:

Das bedeutet, dass in diesem Beispiel Ihre Wohnung in Kilchberg CHF 228.90 teurer sein könnte als in Zürich oder umgekehrt. Wenn Sie in Kilchberg eine Wohnung mit gleichem Preis finden, können Sie sich die Differenz sparen!

Beispiel 3 (Wollerau, Kanton Schwyz)

Der Gleichheitsanteil von 100% im Kanton Schwyz beträgt bei gleichem Einkommen CHF 3'128.00. Berechnet auf 170% ergibt sich für den Kanton CHF 5'319 und für die Gemeinde Wollerau 75%, was CHF 2'347 entspricht. Ohne die Bundessteuer zahlen Sie CHF 7666 und zuzüglich CHF 2'544 Bundessteuer ergeben sich insgesamt CHF 10'210.

Zusammenfassung

- In Zürich City würden Sie insgesamt CHF 15'369 bezahlen.

- Im Kanton Zürich in Kilchberg würden Sie CHF 12'621 bezahlen.

- Im Kanton Schwyz in Wollerau würden Sie CHF 10'210 bezahlen.

Je früher Sie die Kalkulation für sich durchrechnen, desto schneller können Sie aktiv Geld sparen oder es nach Belieben in der Stadt ausgeben, in der Sie gerne leben. Bedenken Sie immer, je höher Ihr Einkommen, desto grösser ist der Unterschied. Vermeiden Sie also voreilige Umzugspläne, ohne sich über die Steuerthematik Gedanken zu machen. Vielleicht sind es auf das ganze Jahr berechnet "nur" CHF 1'000.00 aber auf 10 Jahre berechnet bedeutet das schon CHF 10'000.00, die Sie hätten anders reinvestieren können.

In den letzten Tagen wurden die neuen Krankenkassen-Policen

fürs 2019

versendet.

Somit besteht nun die Möglichkeit, die Krankenkasse zu wechseln.

Gerne unterstützt Obrist Helps mit folgenden Dienstleistungen:

- Analyse der jetzigen Police inkl. Feedback in 60 min.

- Vergleich der Leistungen mit anderen Krankenkassen

- Beratung und aufzeigen von Sparmöglichkeiten

- Hilfestellung beim Ausfüllen des Antrages und der Gesundheitsfragen

- Korrekt Künden

Vielfach sind Sparmöglichkeiten bis zu CHF 50.- oder CHF 100.-

pro Monat

möglich, oder sogar mehr :-)

Als unabhängiger Versicherungsbroker können wir alle gängigen Gesellschaften

anbieten.

(Wir haben unsere Erfahrungen und somit auch unsere Favoriten - im

Umkehrschluss aber auch Kassen die wir aus Gründen des schlechten Services

nicht gerne anbieten)

Obrist Helps legt viel Wert auf eine seriöse Beratung

und einen sinnvollen

Wechsel.

Wenn es keinen Sinn macht zu wechseln, dann raten wir

davon ab.

Überzeugen Sie sich von unserem Fachwissen: Anrufen unter 044 772 14 44

oder schauen Sie sich die etlichen positiven 5* Bewertungen auf Google an :-)

Gerne auch gleich die Police senden auf

info@obrist-helps.ch

An accident can happen to anyone. Even if it's only your own vase, bought from the supermarket, that breaks, the world is still fine and there is nothing special to worry about. But what if it's not your own vase, but the antique vase of the recently deceased mother of your host? That could be expensive. We show you how to insure yourself to prevent damage at third parties.